Welcome to NexusFi: the best trading community on the planet, with over 150,000 members Sign Up Now for Free

Genuine reviews from real traders, not fake reviews from stealth vendors

Quality education from leading professional traders

We are a friendly, helpful, and positive community

We do not tolerate rude behavior, trolling, or vendors advertising in posts

We are here to help, just let us know what you need

You'll need to register in order to view the content of the threads and start contributing to our community. It's free for basic access, or support us by becoming an Elite Member -- see if you qualify for a discount below.

-- Big Mike, Site Administrator

(If you already have an account, login at the top of the page)

Trading: Primarily Energy but also a little Equities, Fixed Income, Metals, U308 and Crypto.

Frequency: Many times daily

Duration: Never

Posts: 5,059 since Dec 2013

Thanks Given: 4,410

Thanks Received: 10,226

Thanks Kevin.

So given that, another option is to recalibrate on the last 10 years of data, or the entire 12 years of data, without any out of sample data?

Final question would you ever trade 2 very similar but slightly different models to get some diversification, or just stick with the one you think is best? Was thinking that since the original model (04-13) has done so well that I might allocate half the position to that, and half the position to the new most recent 10 years (06-15). The parameters will be similar but slightly different.

I would certainly think about trading 2 similar models, instead of trying to pick the "best" one and trading it double size.

You'll get a more average return (you won't get the best return, but you won't get the worst either), but the biggest thing is you save emotional capital by not stressing over "did I pick the best one?" That alone might be well worth the price for "blending" the two together.

I am in the process of reading your book, you did a fantastic job.

Question: given your extensive testing experience, what is the shortest timeframe that you found any profitable system on? For example, did you ever find anything on 5 min? 3 min? 15 min? Or are slippage / cost too prohibitive on that scale?

Thank you!

You are never in the wrong place... but sometimes you are in the right place looking at things in the wrong way.

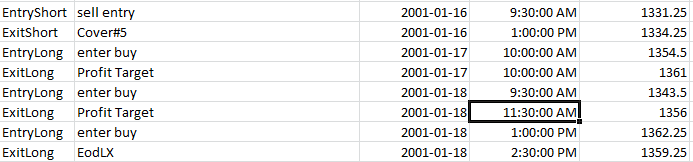

As you can see, the original code is referencing 30M, and I am using 1M bar magnifier to obtain the backtesting results. When I look at my backtesting results (list of trades), the resolution step is 30 minutes. So I don't know whether the trade entered at 9:01AM or 9:28AM.

When I use 1M code to reference 30M logics, I obtain a 1-minute resolution. See below.

As you can see above, I know exactly that the trade entered at 9:03M and exited at 9:13AM. This way I can compare the real trades with the backtesting results to measure slippage, signal accuracy, and reliability.