Welcome to NexusFi: the best trading community on the planet, with over 150,000 members Sign Up Now for Free

Genuine reviews from real traders, not fake reviews from stealth vendors

Quality education from leading professional traders

We are a friendly, helpful, and positive community

We do not tolerate rude behavior, trolling, or vendors advertising in posts

We are here to help, just let us know what you need

You'll need to register in order to view the content of the threads and start contributing to our community. It's free for basic access, or support us by becoming an Elite Member -- see if you qualify for a discount below.

-- Big Mike, Site Administrator

(If you already have an account, login at the top of the page)

Now that it is getting to the holiday time, thought i would take 1 more crack at getting the CL spread analysis right.

There are some limitations to downloading data quickly and its a little labor intensive but once i know what i am trying to achieve I can explore automation.

Lets say we want to analyse the near term 6 month spreads - M18/Z18 and Z18/M19 but i will use M18/Z18 for this discussion

First question I would have is

A) Whether calendar spreads can be mean reverting (like flys) or generally follow the Cl curve or say the 1M spread curve

The answer to that would probably dictate what further analysis is essential

- Should I also compare it with the CL outright curve for 2018?

- Should I compare it to the 1M spreads for 2018?

If mean reverting, would I not compare the 6m spread to the fly curve (M18/U18/Z18 or something else?)

b) Historic Analysis: Assuming we will need to compare it to the same spread for previous years so M17/Z17, M16/Z16 etc

Second Question: I am sure we can superimpose and compare visually but there is probably more value in running statistical regression analysis between the curves

- Am i using polynomial regression or liner is fine?

- Am i comparing the CLES6M8 with not only the same historic spreads but also the outright or 1M spreads?

- I would think there would be need to compare the effect on historic correlation between CL outright and the 6 month spread and extrapolate the value to the current relationship between CL and 6month spreads

(for example in 2016, look at CL curve and the 6month spread in 2016 and use that for 2018?)

Data Gathering:

I can get current and future spreads using CQG RTD but limited to 300 rows (MS RTD limitation).

Also I am not be able to get historic data on the spreads. So I am limited to

- Use CQG RTD to output spread for current/future spreads

- Use download for Sierra historic charts for individual contracts, dump into excel and diff M vs Z (since cannot get historic spread charts but can get 10 year data for outrights)

Third Question: I am assuming i can do the Last price for M vs Last price for Z to come up with the daily spread settlement price

So currently have CLES6M8 (6 month spread M/Z for 2018) and the same 6 month contracts for 16 and 17

Notes:

- My goal is to move away from M/Z to Z18/M19 when it gets close to 50 days to expire of M18

- Conducted calendar and fly analysis for future months and find M, Z are the best months (this was discussed previously.. though H and U are also viable but M/Z are better)

- For exchange flys, i see implied being turned on but volume seems low for 6 and 12 months but very good volume for 2018 1M flys

Ok enough rambling for now.. more later.. once i get some better answers and run some analysis

Thanks to all who could guide me and i am more willing to share with any newbies (we can be the blind leading the blind)

Maybe I will ask a simple question first. If I have an exchange traded spread and open an outright which is an opposite of one of the legs of the calendar spread what happens to the exchange spread? Example I buy CL M18/z18 I.e long M and short Z then I just sell a M18 CL outright separately what happens??

Trading: Primarily Energy but also a little Equities, Fixed Income, Metals, U308 and Crypto.

Frequency: Many times daily

Duration: Never

Posts: 5,059 since Dec 2013

Thanks Given: 4,410

Thanks Received: 10,226

An exchange traded spread isn't a contract in itself, it's a spread between two contracts. If you execute an exchange traded spread what hit's your account are the outright futures involved in the spread.

Trading: Primarily Energy but also a little Equities, Fixed Income, Metals, U308 and Crypto.

Frequency: Many times daily

Duration: Never

Posts: 5,059 since Dec 2013

Thanks Given: 4,410

Thanks Received: 10,226

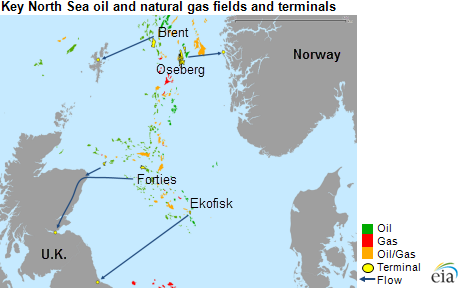

The Brent Price/Index doesn't just represent Brent Crude anymore, it's now a North Sea Basket Index, "BFOE" made up of Brent, Forties, Oseberg & Ekofisk. Today the pipeline that brings Forties onshore was shut down for an estimated 2 weeks.

Now its getting interesting. After SO many bullish news this week, plus bullish invetory data, CL is going down? I can only imagine what will happen when these longs i saw in the last COT report try to exit the market. Together. Quickly. The optimistic target will be 52.80, which is 50% retracement of the last leg up. Popcorn time for me, good luck trading that "OMG" market action.

The Shanghai International Energy Exchange (INE) will allow Chinese buyers to lock in prices using local currency (RMB) and will also allow international traders to trade the contract too. Trading will launch January 18th 2018.

I think this could be interesting if it grows to be of significance as a 3rd benchmark. I wonder what the arbitrage opportunities are like vs other medium sours such as Dubai/Oman?

I have a question regarded disaggregated COT reports on CL. I've always used it just as commercials non commercials, understanding commercials as producers hedging their production, (usually seeing it as when commercials are record short, oil should go down soon)

but if you look at the disagregated reports it seems there is a big difference between producers and swap dealers. ATM it seems the producers are net neutral while swap dealers are record short.

Trading: Primarily Energy but also a little Equities, Fixed Income, Metals, U308 and Crypto.

Frequency: Many times daily

Duration: Never

Posts: 5,059 since Dec 2013

Thanks Given: 4,410

Thanks Received: 10,226

swap dealers buy swaps from producers and then hedge the swap exposure with futures - hence they are nearly always short futures.

Also when looking at the COT reports you have to consider that there are other products that have the same or very similar risk profiles as futures, and as such the COT reports may not be as accurate as you might think.