Welcome to NexusFi: the best trading community on the planet, with over 150,000 members Sign Up Now for Free

Genuine reviews from real traders, not fake reviews from stealth vendors

Quality education from leading professional traders

We are a friendly, helpful, and positive community

We do not tolerate rude behavior, trolling, or vendors advertising in posts

We are here to help, just let us know what you need

You'll need to register in order to view the content of the threads and start contributing to our community. It's free for basic access, or support us by becoming an Elite Member -- see if you qualify for a discount below.

-- Big Mike, Site Administrator

(If you already have an account, login at the top of the page)

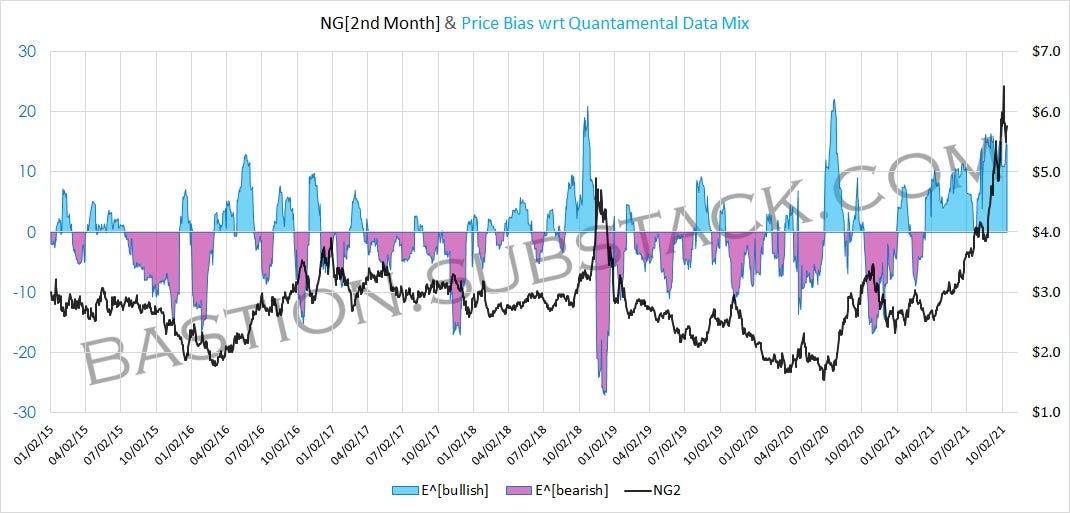

Short term outlook based on COT positions, EIA storage, CPI, is currently fairly bullish into the next month or 2. Though I'm pretty sure we probably didn't need any numbers to be bullish this winter, haha.

Trading: Primarily Energy but also a little Equities, Fixed Income, Metals and Crypto.

Frequency: Many times daily

Duration: Never

Posts: 5,057 since Dec 2013

Thanks Given: 4,399

Thanks Received: 10,225

You called it!

Per John Kemp :-

EU28 gas storage sites have increased inventories by +22 TWh since the start of Oct, the second-largest late-season storage build in the last ten years, and compared with an average build from Oct 1 to Oct 12 of just +14 TWh:

Trading: Primarily Energy but also a little Equities, Fixed Income, Metals and Crypto.

Frequency: Many times daily

Duration: Never

Posts: 5,057 since Dec 2013

Thanks Given: 4,399

Thanks Received: 10,225

23 Days without a margin increase but the next one is here...

NG Margin increase effective COB October 29th, 2021

Maintenance margin's increasing as follows (Note: Non-member initial margin rates will be 110% of these)

Tier 1-3 / Dec21-Feb22 from $6400 to $700 +$600 +9.4%

Tier 4 / Mar22 from $6000to $6500 +$500 +8.3%

Tier 5 / Apr22 from $2800 to $3000 +$200 +7.1%

Tier 6 / May22 from $2100 to $2200 +$100 +4.7%

Tier 7-11 / Jun22-Oct22 from $1950 to $2150 +$200 +10.3%

All other months unchanged.

A naive question, I was never looking when I was briefly trading NG (mostly with naked put options 2 years ago) to European situation or European weather, do you really think that things have changed so much that the situation in Europe can have a significant impact on NG traded at NYMEX? Otherwise why even have a look to the European storage, unless you trade European gas? I start to refollow a little bit this commodity due to the season but Politics (Poutine, Bielorussia etc) coming into the game renders this one even more complicate (already only the weather is a headache).

Trading: Primarily Energy but also a little Equities, Fixed Income, Metals and Crypto.

Frequency: Many times daily

Duration: Never

Posts: 5,057 since Dec 2013

Thanks Given: 4,399

Thanks Received: 10,225

As @myrrdin and @ron99 mentioned, US LNG exports have increased significantly over the last 10 years. With US Natty prices in the Gulf Coast (where most of the export terminals are located) around $5/MMBtu and worldwide prices at $25 for TTF (Europe) and $31 for JKM every drop of LNG that can be exported, will be.

It should be noted, that while we are exporting LNG from the Gulf Coast as fast as we can, during winter we will also be importing LNG. New England is still capacity constrained and can not support itself purely from US pipeline flows. As such places like the Everett LNG Facility in Boston Harbor will be importing LNG, which is also part of the reason that Natural Gas price in Boston (aka Alqonquin City Gate) are about $20/MMBtu for delivery in January despite prices in the Gulf being $5*.

* The Algonquin basis is the price the price spread between Algonquin City Gate and Henry Hub. This can be traded on ICE as product ALQ. For price information go to https://www.ice.com/marketdata/reports/142 and select product ALQ.

I agree that it matters more now than 10 years ago but the question is how much more does it matter for NG traded in NYMEX?

Did I read somewhere that 90% of this 10% of US NG production is anyway for Asia, and almost nothing for Europe and that most of the contracts for Asia are long term contracts with a prespecified price?

So I would be more comfortable going long at the current level of price if the US forecast is clearly bullish, whatever the situation in EU is or will be.

Trading: Primarily Energy but also a little Equities, Fixed Income, Metals and Crypto.

Frequency: Many times daily

Duration: Never

Posts: 5,057 since Dec 2013

Thanks Given: 4,399

Thanks Received: 10,225

In my example the prices in Boston for the peak of winter are $15/MMBtu higher than Henry, as that's the price they get the needed LNG to balance their system. I think you could also make the argument that if we have a cold winter here, and prices do spike that US/Henry prices could spike to the level where we start curtailing exports. I'm not sure what that price actually is but its considerably higher than $5.