Welcome to NexusFi: the best trading community on the planet, with over 150,000 members Sign Up Now for Free

Genuine reviews from real traders, not fake reviews from stealth vendors

Quality education from leading professional traders

We are a friendly, helpful, and positive community

We do not tolerate rude behavior, trolling, or vendors advertising in posts

We are here to help, just let us know what you need

You'll need to register in order to view the content of the threads and start contributing to our community. It's free for basic access, or support us by becoming an Elite Member -- see if you qualify for a discount below.

-- Big Mike, Site Administrator

(If you already have an account, login at the top of the page)

I voted, and thought I would add a comment to continue the discussion aspect... I started an account with 30k for trading. This was cash sitting in another diversified brokerage account that I pulled aside to make sure the "fun money" was held separate. Even though I only really dabble occasionally in futures, the point of starting with that account was to ensure I could daytrade things like SPY and QQQ (not as popular here, I get it)... But, what it has made apparent is that I am incredibly risk averse. A 3 point stop on ES trades is a $150 loss, which is .5% of the account and those still mess with my head for some reason. I've had to instate a "two-trade per day" rule just to ensure I don't either get confident or start revenge trading...

This. It's not about a total size of the account, it's about how much you can tolerate losing on each trade several times in a row without getting emotional about it. It is much more difficult to keep the head cool when you switch from simulation to real money.

To me personally percentages don't work. If I lose $100 and it hurts, even though it's less than 0.05% of my account, I cut my risk even lower. But I trade equities so it's easier to go as low as I want.

I know I'm horribly underfunded, but am at the place where I am having to re-learn to trade, after switching from sim to real money and finding that my emotional reaction to loss is SO much stronger than I'd realized.

So, I am trading as conservatively as I possibly can and am working to cultivate real-money habits that will keep me in the game.

Keeping my account absurdly low keeps me from any revenge trading, as any loss greater than about $500 will mean I have to re-fund myself.

This is very tricky question to answer. Very tricky but you should train in the demo with exact same parameters as you will go live. A problem many make is trading a larger account in the demo and then going live on a much smaller account.

It should be understood there are different ways of looking at day trading. One can look at day trading in terms of drawdown and return. This can be sensible. However, it is also possible to look at day trading as an endeavor that could yield a return consistent enough to provide for a living or at least significant returns on a small account. This is more of a daily risk model, call it the TST or Oneup model. In this style of looking at trading, you don't really think in terms of return and drawdown (drawdown implies a return whereas if you lose the money daytrading, what's that imply? Nothing you just lost the money.) but rather in terms of your daily maximum loss and your potential for gain. Typically, this second way of looking at trading has an objective of very consistent returns. If one is to achieve very consistent returns, then obviously the loss must be minimal, implying that one doesn't need a very large account. Notice, that it is risk endeavor: such day traders may not think in terms of of percentage drawdown or percentage return, even. In order to achieve consistency required, you need to be able to maintain a very high win rate or achieve similar results in some other way. The easiest way I've found to do this is to load size on my best trades. Losing periods are seen as "adjustments" and atypical.

One problem with larger accounts is that it can make one lackadaisical toward taking profits and cutting losses. On the other hand, if you trade a small account, because futures contracts are a fixed size, you won't be able to load/stack the deck in your favor without potentially over leveraging your account. This is not a problem with CFD's and Forex; however.

Method 1 Estimate From Your Existing Trading Method

One way to solve the problem is to, based on your historical performance, determine what you need for a daily loss limit. Because the contracts are fixed size, your daily loss limit will influence how are you are required to trade. Let's assume your daily loss limit is $1,000. Once you determine your daily loss limit, you need to determine your probability of hitting some run of your daily loss limits, a reasonable level is somewhere between 4x and 12x. That suggests an account in the 4k to 12k range plus extra for margin requirements plus extra for any drawdown (run of non maximum loss days).

Method 2 Estimate From Your Account Size

The other way is to work backwards from your account size. The 2% rule is not really meaningful unless you know your win ratio. But, I suspect that it is too conservative to achieve really superior gains. On the other hand, from extensive system testing, I've seen that most systems that work or that I would trade, rarely have a run of more then 12 losses in a row. If we substitute the losses for days, we come up with a number of 8.3%. This is the maximum amount you'd want to risk on your per day but is still probably too high for most. It would yield a 2k daily loss limit. In reality, you'd probably want to cut this by at least in half, but it suggest with a 25k account at a 4% daily loss limit, you can risk around 1k per day. If you can trade your existing methods without needing more then 1k loss limit per day then you would be appropriately capitalized based on this estimate.

Method 3 Estimate From Your Systems Performance

If you trade systems, you can just look at the system performance. Systems tend to require larger stop losses.

----

It is not really possible for me to answer this question but this sounds more then sufficient if you have obtained professional level trading capability and are happy with risking the money. It should be noted: the only reason you need a larger account is so that you can (1) make more per day or (2) because your account is too small to either take the required stop losses for your system or your account is too small to load contracts on your best trades.

The idea you need a huge account is completely false. But, it is true that trading too small of an account can cause problems because of (1) you may not be able to afford keep trading after a not too untypical bad run of losses (forget drawdown for trading-- Don was right), (2) you may not be able to trade in the way that you want, and (3) you may have some performance anxiety knowing you can't afford losing more then a few days. It is very important to understand that most these problems only derive from the fact that futures are fixed notional contracts.

Honestly this belief you have is a concern as such I would suggest: train on the simulator with only 12k account for 3 to 12 weeks. If you can trade it well then you could go live with 12k-15k while preserving the rest.

On the other hand, just to point out, notice that if you came up with at the full 8% risk per day and you run that on a 3k account, you get $240. A tick in ES is $12.50. Due to normal fluctuations, it would be very difficult to trade with less then 3-4 ticks risk, at average 4 ticks risk this yields $50 per trade. You can have up to 5 trades per day but your wins will also be smaller, so you will need more trades per day. If the dominant frequency of your trading information doesn't occur at an agreeable wavelength frequency you will have effective impedance mismatch. So, this influences the type of trades you can take. If you are a discretionary trader, you might be able to adapt to work within these confinements. But for systems, it is very difficult to make any system work with such tight risk parameters in my experience.

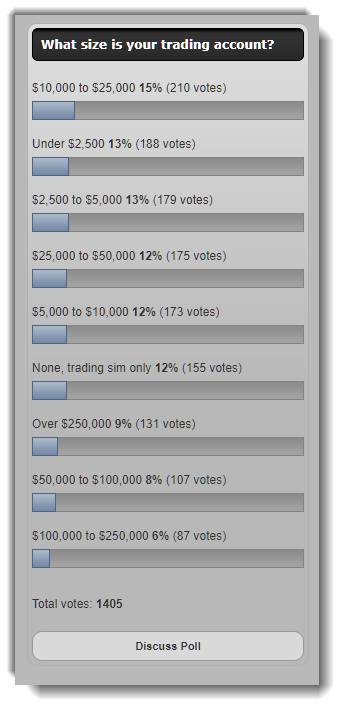

So only 23% of us are using trading accounts that are 50k or greater. This poll kind of also shows what the failure rate is. Also, that at least 77% of us are under funded. Interesting #'s. I'm one of those 77% but I'm still to chicken to allocate more of my funds to trading. I have the money to do so but I don't want to take on a greater $ amount of a loss on one single trade. I feel that I will need at least 3 more months of success before doing that. That is just my guess because it will all be determined on when my emotions can handle an increase in risk.

TPredictor, I am impressed with your knowledge and with the clarity of your text.

Actually, this very issue (assessing position sizes) is what pushed me to a rather algorithmic approach.

You say: " Method 1 Estimate From Your Existing Trading Method

One way to solve the problem is to, based on your historical performance, determine what you need for a daily loss limit. Because the contracts are fixed size, your daily loss limit will influence how are you are required to trade. Let's assume your daily loss limit is $1,000. Once you determine your daily loss limit, you need to determine your probability of hitting some run of your daily loss limits, a reasonable level is somewhere between 4x and 12x. That suggests an account in the 4k to 12k range plus extra for margin requirements plus extra for any drawdown (run of non maximum loss days)."

When you go algo, you must bare with a lot of restrictions and limitations relative to your previous approach. On the other hand, algo gives you some fantastic tools to evaluate things like "position size", "risk assessment", etc.

If you know how to do algo the right way, for your "Method 1" your "historical performance" can be replaced with "walk-forward backtest" in order to fine-tune both your "Expected Daily Loss Limit" and your "Multiplication rate" (which is between 4x to 12x).

With the use of Montecarlo techniques, you can arrive to an assessment like this:

"If I start trading one ES contract today, my average expected 'worst loss' will be $1,600.00 and my expected 'bankruptcy loss' will be $2,400.00".

"Bankrupcy loss" is the amount which reveals that your strategy "broke" and there's no use keeping trying. If you achieve this loss, you must retire that specific strategy and record your loss as permanent.

Montecarlo analysis gives you the "worst expected loss for, let's say, 99% of all possible scenarios" (which is the bankruptcy loss).

This finally dictates how much money per contract (additional to margin) you must keep and also the possible advantages of implementing of a "variable positions size" policy, (like Kelly Criterion or the such).

Algo trading steals you much of your improvisation skills, common sense, etc. Therefore, in order to compensate, the things that it offers as additional resources must be explored with all eagerness.