Welcome to NexusFi: the best trading community on the planet, with over 150,000 members Sign Up Now for Free

Genuine reviews from real traders, not fake reviews from stealth vendors

Quality education from leading professional traders

We are a friendly, helpful, and positive community

We do not tolerate rude behavior, trolling, or vendors advertising in posts

We are here to help, just let us know what you need

You'll need to register in order to view the content of the threads and start contributing to our community. It's free for basic access, or support us by becoming an Elite Member -- see if you qualify for a discount below.

-- Big Mike, Site Administrator

(If you already have an account, login at the top of the page)

I used this stategy (Export Data.zip) to export hour data from NT to a csv file and wanted to see how it would handle the transition from one contract to another for NQ (mergebackadjusted). I was looking to see if it really exported the data "back adjusted". But what I found I think may be a bug. There are 3 hours missing in the data at the end of the old contract (see attachment). From 0021 to 0100 the next day (first hour of rollover contract). Can someone explain this to me? I hope this is not what NT means by "merge back adjusted" - just lop off a few hours.

Can you help answer these questions from other members on NexusFi?

@Fat Tails is a master at how NT handles back adjusted/rollover. So I've shouted at him to come take a look, he probably knows the answer and can help you.

All – I got a bunch of data off this forum yesterday which I will be using to do some probability analysis of some of the setups I use. This is excellent stuff and in return I would like to give something back.

This is a difficult subject. I have exported my backadjusted data for NQ 03-11 from 01-01-2009 up to now. So here are the results.

First of all, the export strategy works well, you can easily export a text file and convert it to Excel. Thank you @MXASJ for this tool.

-> I have different values for Dec 10 2009 compared to those shown above. I do not have any value above 1,800. This points to different offsets or a different backadjustment method.

-> I use a session template, which is in line with market hours. My trading session starts at 3:30 PM CT (night session) and 8:30 AM CT (real trading hours). You obviously did not use a session template adapted to NQ, but something else.

If we really want to compare our results, we will first have to agree on identical market hours and offsets. I do not pretend that my data is clean, as I am not trading NQ. I simply exported what I had in my data base without checking any details.

Bugs

-> The data export only started on January 5, 2009. The data for January 2, 2009 and for part of January 5, 2009 is missing. In practice you would need to export the data starting somewhere from December 2008 and then delete the data for December manually.

-> The last candle of my database is missing, that is the closing candle of last Friday. I have seen things like this before with NinjaTrader. You need to add the last candle manually.

Rollover Dates

I have found that the exported data series correctly reflects the mergebackadjusted data in my data base.

I attach the exported data, so that you can compare the values.

Hi, I posted this problem in the "multicharts" thread but I've been searching for a solution and this thread seems to be the closest fit.

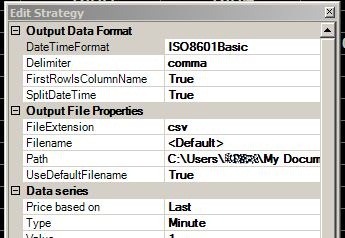

When using the Export data strategy I get the message "Invalid path. Please check your Path and Filename variables". I've tried changing the path to "C:\Documents" but that didn't help. I left eveything else as default.

Do I change session template to "forex"?

Thanks

Do you have a folder named "Documents" at the root of your C drive? That error usually indicates the path or destination folder is not valid, and if you have an Output window open you should see the full error message.

If you were looking to save it to your "My Documents" folder, the path should be C:\Users\<user name>\My Documents or C:\\Users\<user name>\My Documents. Both will work.