Welcome to NexusFi: the best trading community on the planet, with over 150,000 members Sign Up Now for Free

Genuine reviews from real traders, not fake reviews from stealth vendors

Quality education from leading professional traders

We are a friendly, helpful, and positive community

We do not tolerate rude behavior, trolling, or vendors advertising in posts

We are here to help, just let us know what you need

You'll need to register in order to view the content of the threads and start contributing to our community. It's free for basic access, or support us by becoming an Elite Member -- see if you qualify for a discount below.

-- Big Mike, Site Administrator

(If you already have an account, login at the top of the page)

No, i worked with the nonlinear workbook (g****e,rapids***e). the code is at the time limeted. with bearcave I do not get good results

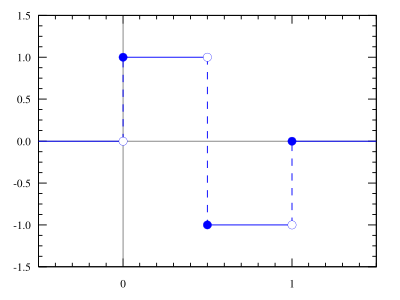

some things must be changed. now i count only 54 bars back and not the full series. the other question is how i interpret the wavelet correctly. i mean the haar wavelet use only 1,0,-1 for this. For more infos i used wiki, in this case my math skills are sleeping well.

wh

Can you help answer these questions from other members on NexusFi?

They are a bit hard to understand at first but it is a very powerful methodology for time series analysis, worth spending some time to learn IMHO.

BTW with Haar transform you don't have to worry about boundary conditions and edge effects that I mentioned previously. The only thing you must worry about in that case is that you use an undecimated version of the transform (no downsampling).

StationaryWT, MODWT, Translation Invariant WT, A'Trous algorithm are all different names for the undecimated transform.

You can get very good denoising result using only the Haar transform provided that you use good thresholding method. Check this research paper which gives simple version of the algorithm: https://www.unige.ch/fapse/mad/renaud/papers/KalmanWavelet.pdf

True, wavelets are not that useful for discretionary trading, it is very powerful for algorithmic trading due to its power of feature extraction which makes pattern recognition much easier.

I skimmed through the research paper you linked above, only problem is their method can't be used in real time because they use future data in their calculations. Here is another similar paper which uses wavelets, fuzzy logic and neural network together for forecasting exchange rates.

This one I have implemented myself and can verify that the approach works quite well =)