Welcome to NexusFi: the best trading community on the planet, with over 150,000 members Sign Up Now for Free

Genuine reviews from real traders, not fake reviews from stealth vendors

Quality education from leading professional traders

We are a friendly, helpful, and positive community

We do not tolerate rude behavior, trolling, or vendors advertising in posts

We are here to help, just let us know what you need

You'll need to register in order to view the content of the threads and start contributing to our community. It's free for basic access, or support us by becoming an Elite Member -- see if you qualify for a discount below.

-- Big Mike, Site Administrator

(If you already have an account, login at the top of the page)

track volume on a long-term time-of-day basis (i.e. avg or med cumulative vol at 8:30, 9:00, 9:30, etc)

compare current time-of-day volume to the tracked avg / med (i.e. today's 8:30 vs 10-day avg at 8:30, etc)

further compare current cumulative volume by day of week

Is anyone aware of a study that provides this type of data? I know I can come up with most of the data within a spreadsheet, but unsure how smoothly I can translate it into a viable SC study. Also, I don't know how I would pull off the day-of-week element.

Edit: I'm thinking it's possible to somehow re-engineer the Cumulative Sum Of Study to do these things but I wouldn't know how to go about it.

Thanks, in advance, for any thoughts on how this might be accomplished.

Take care -

omni

Luck is what happens when preparation meets opportunity. ~ Seneca

Can you help answer these questions from other members on NexusFi?

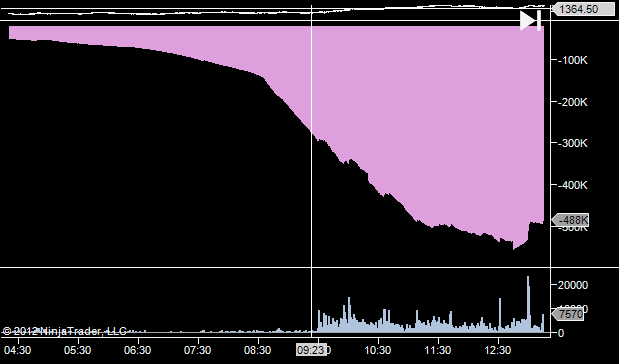

This shows relative cumulative volume for the time of day - you can see we started the afternoon with 488k less contracts traded than normal.

If it's moving down volume continues to be below average.

If it's moving up, volume is above average.

If it's flat, volume is now average.

You can have this moving down to 10am, for instance when there's a release everyone is waiting for. At that point it'l be below average. If it then flattens out, it'll still be below average in total but we will have reverted to mean.

It's direction that is key more than the actual number of contracts +/- for the day.

Omni correctly uses Sierra Chart. I haven't seen this. I can try to do it later in the week if someone doesn't beat me to it. You may have to send me a reminder PM if I don't respond by next week, really.

I'm using a spreadsheet to display these data for 30-minute and 60-minute time slots. I use a 5-day average.

These data could easily be used to plot them on a chart.

In my opinion you need to plot three values:

current volume (no problem),

average/median volume for this time-slot and

a projected volume based upon the current volume.

For the bar on the hard right edge the first two are not enough, you want to compare current volume to its average/median.

I have not looked at volume differentiated by type of day. But since range shows some differences based upon type of day this may be true for volume too.

Thanks for the input, but, as vegasfoster indicates, I'm using Sierra so I can't use Ninja indicators.

Sounds good And if all it takes is sending a reminder next week, you've got a deal!

Excellent effort @FGBL07 Am I mistaken or does your spreadsheet exclude cumulative time-slot volume information? For example, the 9:30 info will be the current and average volume during that 30 (or 60) min time-slot but not total volume for the day at the close of the 9:30 time-slot. Either way, thanks for your comments.

Also, you are absolutely correct - I have seen a few similar discussions on SC but haven't quite found the scenarios I'm looking for. It could just be a matter of not hitting on the right search terms yet.

Still tinkering away here .... but it won't hurt my feelings if @vegasfoster beats me to it

Luck is what happens when preparation meets opportunity. ~ Seneca

I wrote this for Ninjatrader, which allowed for day of week and showed relative volume compared to an average or median. But in NT I did it by adding another data series; in SC I'm not sure this is the best way to go. I will use a little time off today that I would normally be trading and see what I can do, but SC code is still a little new to me so it may take a while.

Sounds good, fellas. Thanks for the interest and the efforts

My eventual goal is to be able to filter by day types. Take trend days as an example. If we see about 20% of the time the ES has a trend day, what typically happens the day after trend days? Is there a condition or day type that occurs 70% or 80% of the time in the session following a trend day? And what about the more common day types, like neutral or variation of a normal? Clearly, there is some subjectivity in defining day types (or opening types), but I'm thinking it could be valuable to have some idea of what frequently happens following certain market conditions.

Luck is what happens when preparation meets opportunity. ~ Seneca

Thanks for clarifying

Thanks for clarifying