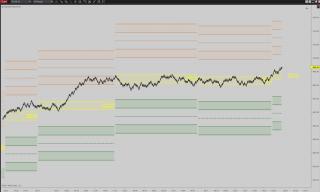

Description: Average daily range zones based on daily ATR and percentage of standard deviation of daily ATR(1) over lookback period.

Important Note: Do NOT put this on an intraday chart with Tick Replay on. It will attempt to download 300 days of tick data. Trust me, you don't want that. It doesn't matter if you set 'Daily Bar Lookback' at a low value. If you do want to put this on an intraday chart with Tick Replay on, I suggest that you go into the code and change the second data series from 300 to something that is acceptable to you and recompile. Sorry, I didn't consider this issue during design and is something that just slipped through the testing process. My apologies.

Following are the calculations for this indicator:

Open = ETH Open

ATR = ATR(Daily, Lookback)[1]

Breadth = StdDev(ATR(Daily, 1), Lookback)[1] * StdDevBreadthMultiple (used to define zone width)

Upper Outer Zone: Open + ATR * 1.00 +/- Breadth

Upper Mid Line : Open + ATR * 0.75

Upper Inner Zone: Open + ATR * 0.50 +/- Breadth

Open Zone : Open +/- Breadth

Lower Inner Zone: Open - ATR * 0.50 +/- Breadth

Lower Mid Line : Open - ATR * 0.75

Lower Outer Zone: Open - ATR * 1.00 +/- Breadth

Features:

1) Can have up to 300 days of daily bars for calculations while only having 1-2 days of intraday bars on the chart (default=252 days)

2) Option to adjust breadth of zones with StdDev Breadth Multiple (default=.2, 0=no zones)

3) Option to show ATR% for day relative to ATR over lookback period. Also, shows days range.

Notes:

1) Only applies to intraday bar charts

Please DM me if you find any issues.

Category NinjaTrader 8 Indicators and More

|

|

|