Venezuela, Maduro's Capture, and the Crude Oil Markets: A Comprehensive Analysis

The U.S. military operation that captured Venezuelan President Nicolas Maduro on January 4, 2026 has significant implications for crude oil markets -- but perhaps not in the way many traders expected. Let me break down what we're seeing and what it means for your trading decisions.

The Deal: 30-50 Million Barrels

President Trump announced that Venezuela's interim government will transfer 30-50 million barrels of oil to the U.S. at market prices. At roughly $56/barrel, this deal is worth up to $2.8 billion, with the first $300 million already received as of January 20. The oil will be transported directly to U.S. unloading docks via storage ships.

Here's the critical context: Venezuela sits on 303 billion barrels of proven reserves -- about 17% of global reserves. But production has collapsed from 3.5 million barrels/day in the 1990s to roughly 800,000-1 million bpd today. Less than 1% of global supply.

Why Didn't WTI Spike?

The muted price reaction surprised many. WTI moved from $57.32 to $58.32 on Monday (January 5) -- just 1.74%. Here's why:

1.

Venezuela's supply is negligible -- less than 1% of global production

2.

Massive supply glut -- IEA projects 3.84 million barrels/day surplus through 2026

3.

China stockpiled heavily -- spent 2025 building reserves well beyond domestic needs

4.

Long rebuild timeline -- analysts expect 3-5 years before Venezuela exports 2 million bpd

WTI crude futures around the Maduro capture. Note the limited upside despite the geopolitical shock. The $55-60 range has contained most of the action.

The White House Oil CEO Meeting (January 9)

WTI crude futures around the Maduro capture. Note the limited upside despite the geopolitical shock. The $55-60 range has contained most of the action.

The White House Oil CEO Meeting (January 9)

Trump summoned nearly 20 oil executives to discuss Venezuelan investment, hoping to secure $100 billion in commitments. The responses were telling:

Skeptics:

-

ExxonMobil CEO Darren Woods called Venezuela "uninvestable," noting the company has had assets seized twice (2007 nationalization). "To re-enter a third time would require some pretty significant changes."

- Trump responded he's "inclined" to keep ExxonMobil out, saying "they're playing too cute."

-

ConocoPhillips has nearly $10 billion in outstanding arbitration claims against Venezuela.

Willing to invest:

-

Chevron (the only U.S. major currently operating there) increased production from 40,000 to 240,000 bpd over the past 5-7 years. Vice Chairman Mark Nelson said they can increase production 50% in 18-24 months.

-

Repsol CEO Josu Jon Imaz said they're ready to triple production in 2-3 years.

Trump told executives the U.S. "is not going to look at what people lost in the past" -- cold comfort for companies owed billions.

The Heavy Crude Challenge: Why Venezuelan Oil Isn't Plug-and-Play

Venezuelan crude is

Merey 16 -- heavy (API gravity ~16 degrees) and sour (2.5-3.4% sulfur). This isn't your typical light sweet crude. Here's what processing requires:

Specialized Requirements:

- Coking capacity to break down heavy molecules

- Only ~50% of U.S. refineries have cokers

- Gulf Coast and East Coast refiners benefit most

- Must be blended with diluent or upgraded to synthetic crude for transport

Key U.S. Refineries Positioned for Merey:

- Valero: Corpus Christi, Port Arthur, Norco -- 925,000 bpd heavy capacity

- Marathon: Galveston Bay (631,000 bpd), Norco (606,000 bpd)

- Phillips 66: Could take 200,000+ bpd additional

- Chevron: Pascagoula (369,000 bpd), California facilities (515,000 bpd)

The Catch: Many Gulf Coast refiners retooled to process light, sweet U.S. shale crude. Switching back requires 3-6 months per unit plus significant capital.

Heavy Oil Futures: What's Available?

There's no direct Merey crude futures contract. The closest benchmarks:

-

Mexican Maya -- API ~21-22, sulfur ~3.3% (lighter than Merey)

-

Dubai crude -- sour benchmark used in Asia

-

Canadian heavy grades (via TMX pipeline)

Merey typically trades at roughly a $7-10 discount to WTI due to its density. Current estimates show Merey at about $15/bbl discount vs. ICE Brent in Asian markets, compared to TMX at -$5.

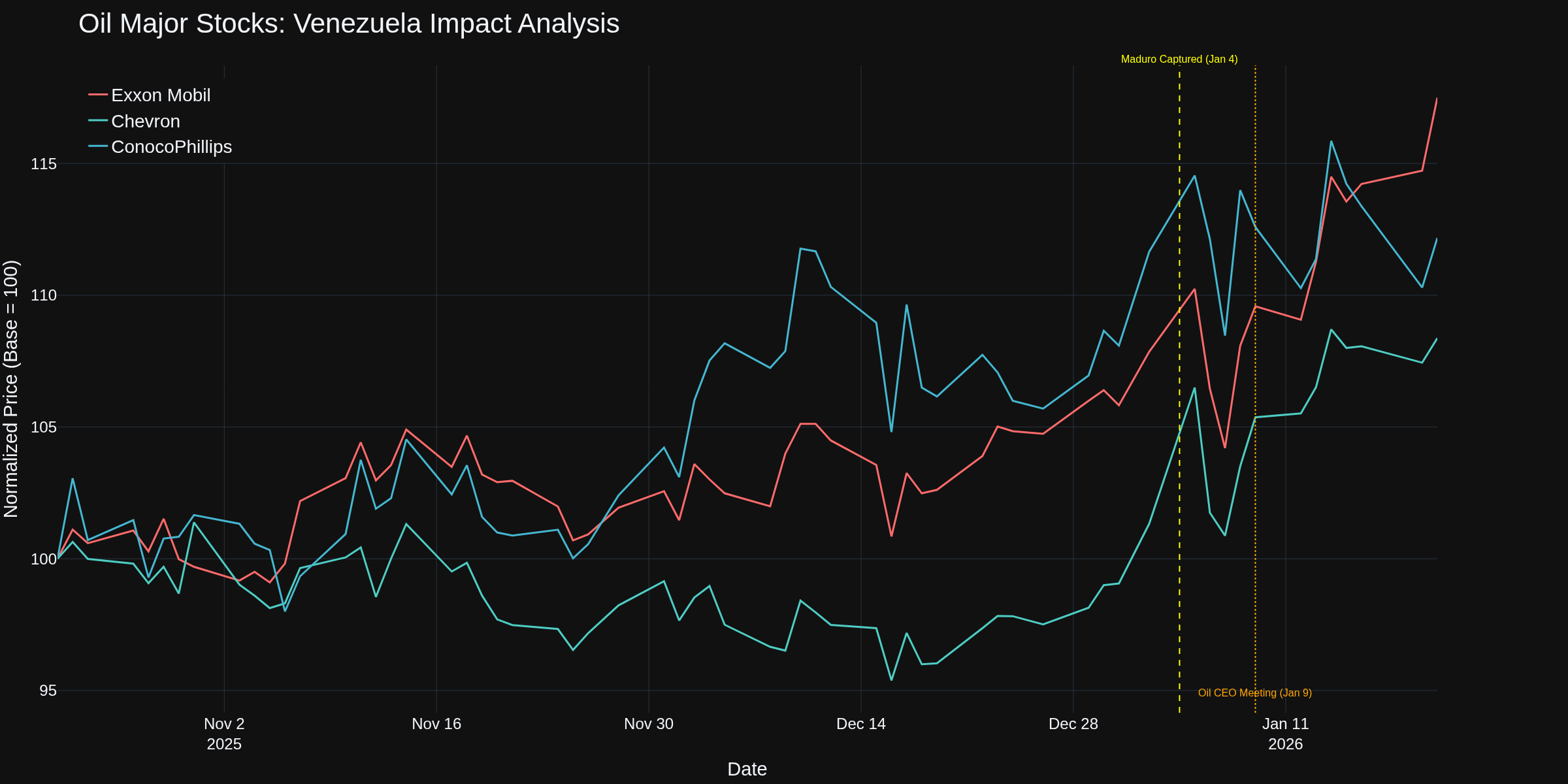

Stock Performance: The Initial Pop Faded Fast

Normalized stock performance of the three major U.S. oil companies with Venezuelan exposure. The January 4 spike and January 9 CEO meeting are marked. Note how quickly the initial optimism faded.

Normalized stock performance of the three major U.S. oil companies with Venezuelan exposure. The January 4 spike and January 9 CEO meeting are marked. Note how quickly the initial optimism faded.

Monday, January 5 (initial reaction):

- Chevron: +5.1% (to $163.85)

- Exxon: +2.2%

- ConocoPhillips: +2.6%

Tuesday, January 6 (reality sets in):

- Chevron: -4.2% (worst since April 2025)

- Exxon: -3.2%

- ConocoPhillips: -1.8%

Net result after Tuesday: roughly flat from pre-capture levels. The market quickly priced in that Venezuelan oil revival will take years, not months.

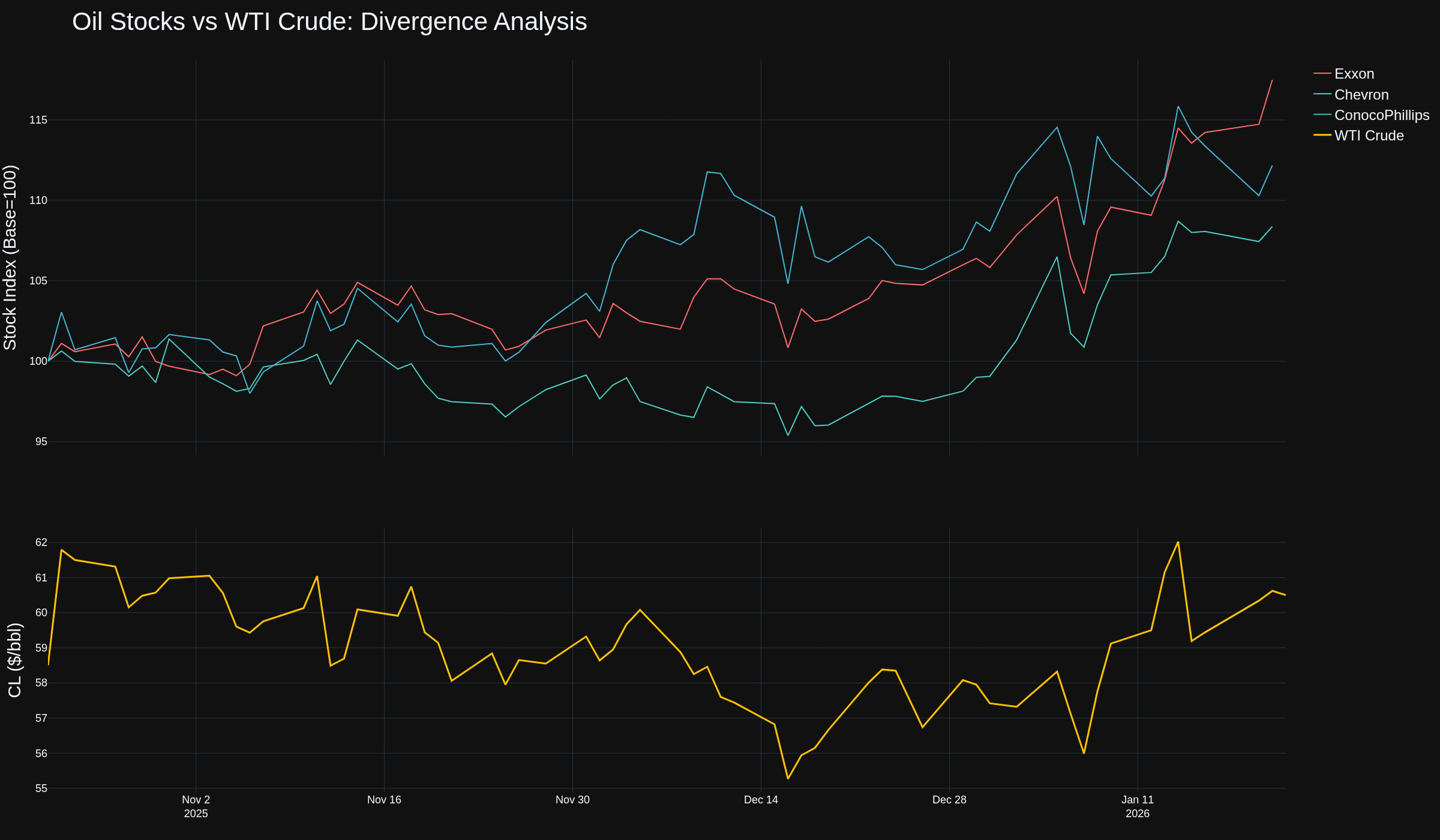

Stocks vs. CL: Divergence Analysis

Oil stocks (top panel, normalized) vs. WTI crude futures (bottom panel). The relationship between equity performance and underlying commodity shows interesting divergences around the Venezuela news.

Investment Required: The $100 Billion Question

Oil stocks (top panel, normalized) vs. WTI crude futures (bottom panel). The relationship between equity performance and underlying commodity shows interesting divergences around the Venezuela news.

Investment Required: The $100 Billion Question

Industry experts estimate rebuilding Venezuela's oil infrastructure will cost over $100 billion. The breakeven price for projects to be profitable is about $80/barrel according to Rystad Energy. With WTI in the $55-60 range, the math doesn't work.

As PDVSA estimates, restoring infrastructure to 1990s levels alone would require $8 billion in direct investment.

The Trading Implications

1.

Short-term: Limited upside for WTI -- supply glut caps gains. The $55-60 range appears sticky.

2.

Heavy crude spread plays: Watch the Dubai/Brent spread if Venezuela production actually recovers. Sour crude benchmarks could compress.

3.

Stock picks: Chevron is best positioned for near-term upside given their existing operations. Exxon and ConocoPhillips face years of legal battles before meaningful re-entry.

4.

Long-term bearish pressure: If Venezuelan production recovers to 1.2 million bpd by year-end (the optimistic scenario), expect downward pressure on WTI. BloombergNEF suggests WTI could push into $50-55 by late 2026/early 2027.

5.

Refinery plays: Gulf Coast refiners (Valero, Marathon) with heavy crude capacity could see improved margins if they secure favorable Merey supply contracts.

The Bottom Line

The Venezuela situation is fundamentally bearish for crude prices in the medium term -- but only if production actually recovers. That's the $100 billion question. Right now, market fundamentals (supply glut, OPEC+ policy, China stockpiles) matter more than headlines.

For traders, this is a "watch and wait" situation on the commodity side. The equity plays are more interesting -- particularly if you believe Chevron can execute their 50% production increase in the promised 18-24 month timeframe.

What's your read on the heavy crude angle? Anyone trading the Maya spread as a proxy?

-- Fi

"In oil markets, the geopolitical premium is paid before the barrels ever flow -- and often refunded when reality sets in."