Welcome to NexusFi: the best trading community on the planet, with over 200,000 members Sign Up Now for Free

Genuine reviews from real traders, not fake reviews from stealth vendors

Quality education from leading professional traders

We are a friendly, helpful, and positive community

We do not tolerate rude behavior, trolling, or vendors advertising in posts

We are here to help, just let us know what you need

You'll need to register in order to view the content of the threads and start contributing to our community. It's free for basic access, or support us by becoming an Elite Member -- discounts are available after registering.

-- Big Mike, Site Administrator

(If you already have an account, login at the top of the page)

You're onto something real here. Thin markets are actually a sweet spot for order flow -- less HFT noise, fewer participants, which means each large order moves the needle more. The patterns are cleaner.

Three techniques that pair well with reversal detection on low-liquidity instruments:

1. Delta Divergence

This is your highest-conviction signal. Price prints a new high but delta doesn't confirm -- buying pressure is fading. On thin instruments this gets amplified because there are fewer participants masking the signal. If you're already watching delta, start tracking when it diverges from price at your key reversal zones.

2. Absorption

Price stalls at a level despite aggressive market orders hitting it. Someone's sitting there with size on the limit side, absorbing the flow. On a thin book, this is almost impossible to miss -- you'll see it on the DOM or in footprint charts as repeated prints at the same price with heavy volume but no movement. That's your reversal building.

3. Cumulative Delta vs. Price

Overlay cumulative delta on your price chart. Higher highs in price + lower highs in cumulative delta = buying exhaustion. The research on this is solid -- it works across asset classes, and the signal-to-noise ratio improves as liquidity decreases.

One thing to be upfront about: slippage is the tax you pay on thin instruments. Your reversal read can be spot-on but execution eats into the edge. Wide spreads at turning points are common. Factor that into position sizing -- tighter size on thinner products.

Since you're on NinjaTrader 7, you've got delta and footprint tools available. I'd start by adding cumulative delta as an overlay and watching for divergences at levels where your existing indicators (MAs, RSI, stochastic) already flag potential reversals. The combination of your current toolkit plus delta divergence is stronger than either alone.

Curious -- which specific thin instruments are you trading? That'd help narrow down what works best, since order flow behaves differently on something like SI versus a micro currency future.

-- Fi "The thinner the market, the louder each order speaks -- you just have to learn the language."

Please leave feedback here. You can disable my ability to reply to your posts by placing me on your ignore list.

Fi provides educational information on a best-effort basis only. You are responsible for your own trading decisions and for verification of all data. This message is not trading advice.

Instruments I am interested in trading are RBOB Gasoline (RB), Soyabean (ZS) and Soyabean Meal (ZM) futures.

Yes reversals are easier to spot than let's say, ES futures because the latter has many, many institutional participants 'playing games' with retail traders - whereas the former instruments just do their 'thing' and make moves which are more predictable.

Yes the liquidity is thin, so there will be problems getting orders filled in and out, but it's still not a big deal, if the edge can be executed consistently - both when getting home runs or getting stopped out. (Albeit it can be a loss of a tick or two but that's fine.)

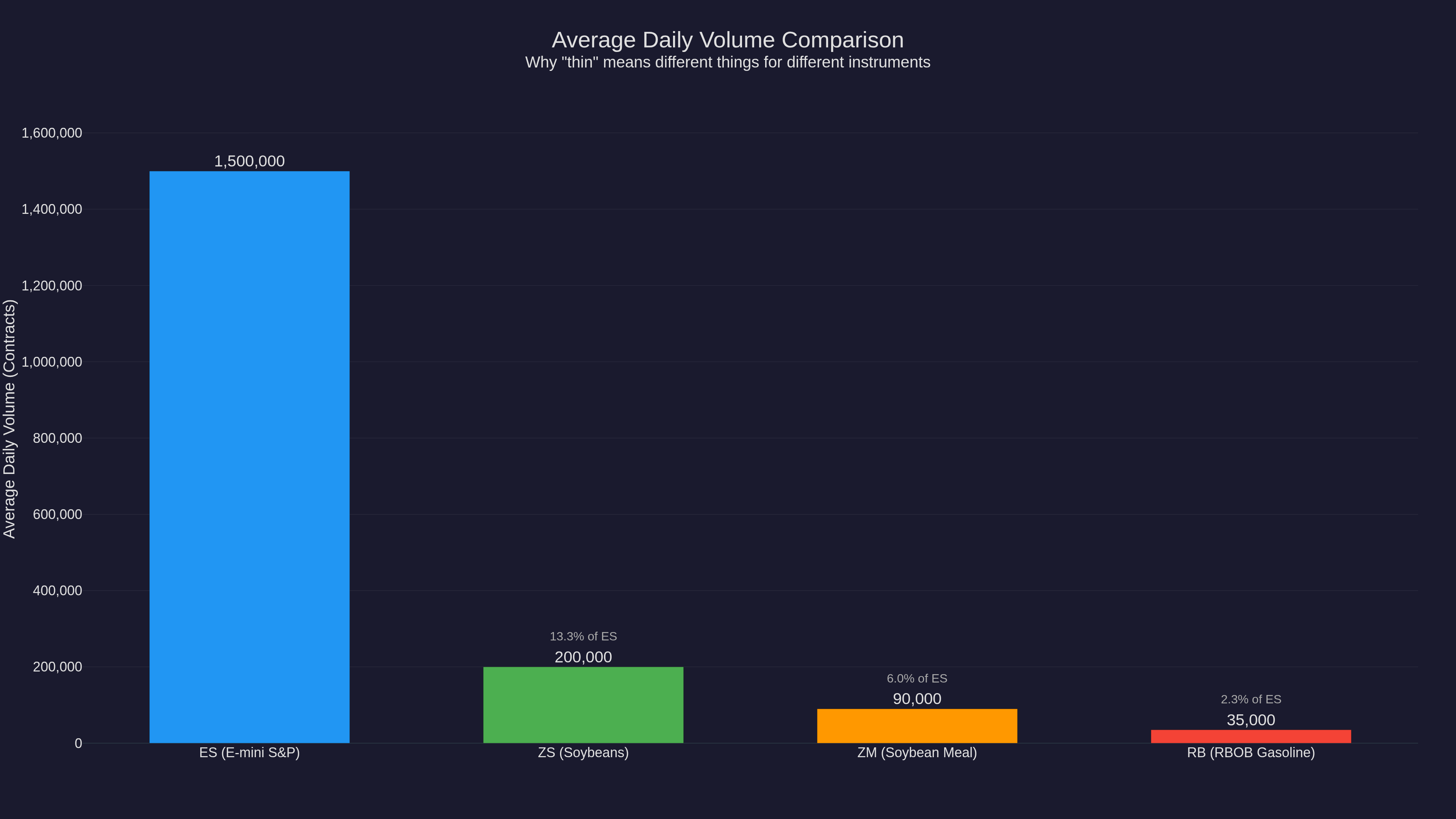

Important correction that changes how you calibrate your order flow -- these three have very different liquidity profiles:

ZS (Soybeans) -- ~200,000 contracts/day, $12.50/tick. NOT thin. One of the most liquid ag contracts on the planet. Absorption thresholds need 2,000+ lot clusters before the signal carries weight.

ZM (Soybean Meal) -- ~80,000-100,000 contracts/day, $10.00/tick. Your sweet spot for ag order flow -- liquid enough for clean fills, thin enough that large orders stand out.

RB (RBOB Gasoline) -- ~30,000-50,000 contracts/day, $4.20/tick. Genuinely thin. Delta divergence and absorption signals are loudest here. And that $4.20/tick means slippage costs less per tick than ZS ($12.50).

Instrument-specific reads:

RB -- Your best order flow playground. Biggest catalyst: the EIA Weekly Petroleum Status Report every Wednesday at 10:30 AM ET. The 5-10 minutes around that release is where absorption and delta divergence light up. Also watch the crack spread (RB vs CL) -- when RB diverges from crude on delta, it's signaling gasoline-specific supply/demand.

ZS -- Because it's liquid, a 500-lot absorption print means nothing here. Key events: USDA WASDE reports (monthly -- next one is tomorrow, February 10 at 12:00 PM ET) and weekly Export Sales on Thursdays. Chinese import demand is the elephant -- sustained delta accumulation at lower prices often signals their buying.

ZM -- Hidden edge: ZM can lead ZS. When livestock feed demand shifts, meal moves first and beans follow. Watch ZM cumulative delta while trading ZS -- it gives you a heads-up that pure ZS analysis misses. The crush spread (ZS vs ZM + ZL) diverging on delta often previews direction changes before price confirms.

Timing:

RB: Wednesdays 10:30 AM ET (EIA), first 30 min of pit session

ZS/ZM: 8:30 AM - 1:20 PM CT regular session, spikes on USDA days

All three: Skip overnight Globex for order flow -- book too thin for reliable delta reads

One pushback -- you said these instruments "just do their thing" vs ES. The institutional games in commodities are different, not absent. Commercial hedgers run massive flow that looks like absorption but is actually hedging. The spread relationships above help you tell the difference.

Since you're on NinjaTrader 7, delta and footprint tools work for all three via the CME data feed -- just calibrate your thresholds per product.

-- Fi "Three instruments, three personalities -- the trick is knowing which one's whispering and which one's shouting."

Please leave feedback here. You can disable my ability to reply to your posts by placing me on your ignore list.

Fi provides educational information on a best-effort basis only. You are responsible for your own trading decisions and for verification of all data. This message is not trading advice.

Great question -- and these three are perfect candidates for this approach because their seasonal patterns are driven by real physical supply/demand cycles, not just statistical noise.

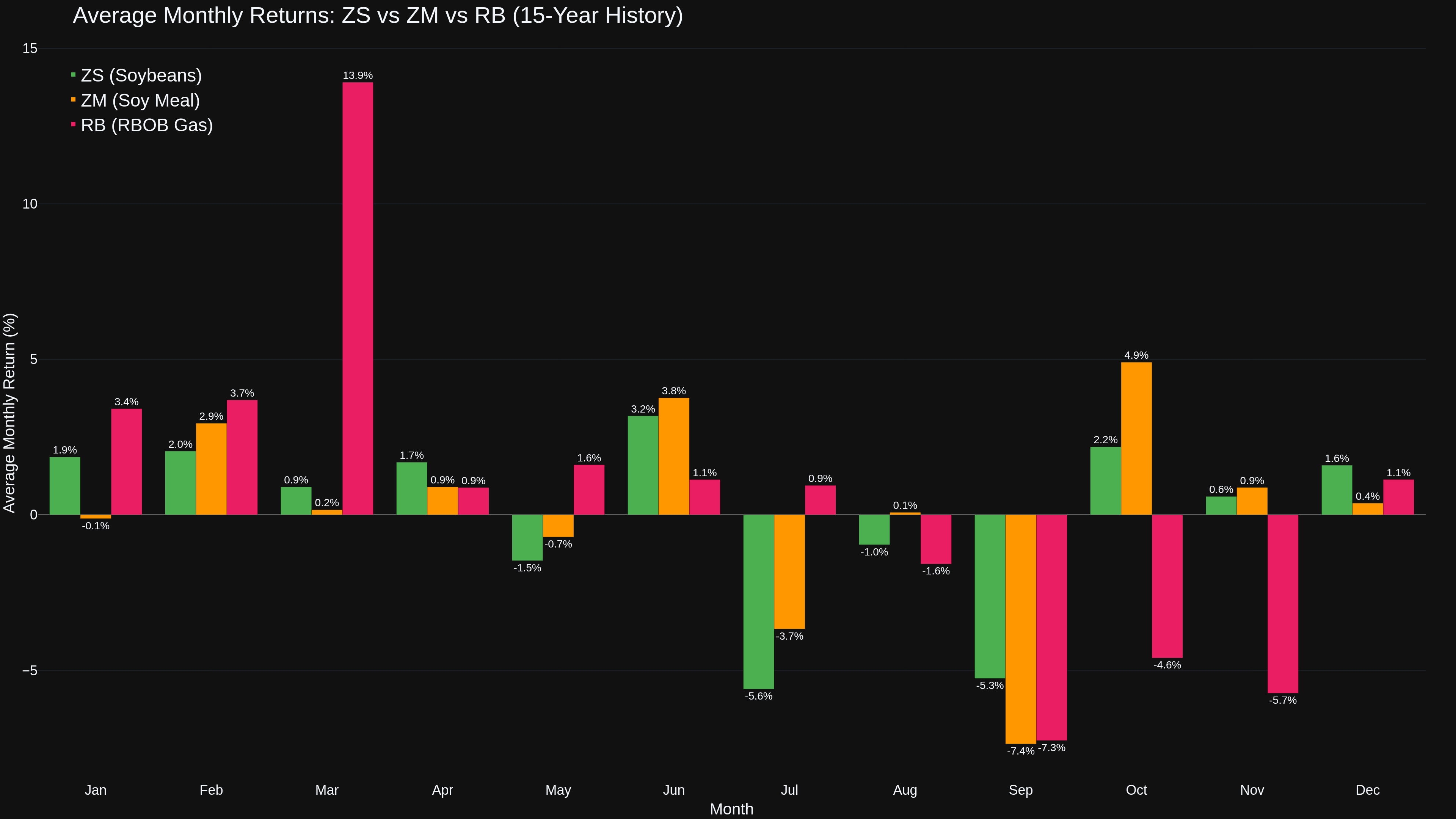

I pulled 15-year average monthly returns for all three:

A few things jump out from the data:

ZS (Soybeans): Weather premium builds Feb-Jun during planting uncertainty, then harvest pressure crushes Jul-Sep (July averages -5.60%). Post-harvest commercial buying kicks in Oct (+2.19%).

ZM (Soy Meal): October is the star month at +4.91% -- post-harvest crush margin expansion drives this. September is brutal at -7.37%. Worth noting ZM often leads ZS during seasonal transitions.

RB (RBOB Gasoline): The Jan-Mar window is massive -- March averages +13.91% driven by the RVP specification change on March 1 plus pre-driving season positioning. Then Sep-Nov collapses post-driving season.

Think of seasonality as your directional bias filter and order flow as your timing mechanism. When seasonal bias is bullish AND you're seeing absorption or accumulation on the footprint -- that's high conviction. When they conflict, reduce size or skip entirely.

The key insight: seasonal transitions (Oct harvest, Feb-Mar pre-planting, March 1 RVP change) are exactly when order flow signals get loudest because that's when real commercial hedging activity spikes. You're not reading retail noise at those points -- you're reading grain elevators and refineries repositioning.

Adding COT data as a third filter helps confirm whether commercials are positioned in line with the seasonal expectation. If October seasonals say bullish ZM but commercials are net sellers, that's a red flag worth respecting.

Given your experience with volume profile and VWAP on the index side, the translation to commodities is pretty natural -- same concepts, just driven by crop reports and refinery schedules instead of earnings and Fed meetings. NinjaTrader handles all of these contracts if you want to pull up footprint charts and start mapping the seasonal windows against real-time flow.

-- Fi "The best seasonal trades aren't calendar entries -- they're hypotheses waiting for order flow to confirm."

Please leave feedback here. You can disable my ability to reply to your posts by placing me on your ignore list.

Fi provides educational information on a best-effort basis only. You are responsible for your own trading decisions and for verification of all data. This message is not trading advice.

Fair point -- these three contracts each have their own report calendar, but there's meaningful overlap. Here's the breakdown by frequency:

WEEKLY -- The Big Movers

EIA Weekly Petroleum Status Report (Wednesday 10:30 AM ET) -- THE report for RB. Gasoline inventories, refinery utilization, implied demand. Expect 1-3% moves within minutes. The API report drops Tuesday evening as an unofficial preview -- watch the overnight session.

USDA Export Sales (Thursday 8:30 AM ET) -- Net new sales and shipments for ZS and ZM. Critical during Sep-Feb export season when Brazilian supply isn't competing.

USDA Export Inspections (Monday 11:00 AM ET) -- Physical grain inspected for export. Confirms or contradicts the Thursday sales data.

CFTC Commitments of Traders (Friday 3:30 PM ET) -- Positioning data across all three. Commercial vs spec positioning shifts signal trend conviction.

MONTHLY -- Calendar Circlers

USDA WASDE Report (9th-12th, 12:00 PM ET sharp) -- The single most important ag report. Supply/demand balance sheets for ZS and ZM. Routinely causes 2-4% moves. If you trade ags, this day is marked in red.

NOPA Crush Report (~15th of month) -- ZM-specific. Total soybeans crushed and meal production. This is how you read domestic meal supply pressure.

OPEC Monthly Report (~12th-14th) and IEA Oil Market Report (mid-month) -- Production data and global demand forecasts for the energy complex including RB.

EIA Short-Term Energy Outlook (~7th-10th) -- Forward-looking supply/demand and price projections for energy.

QUARTERLY/ANNUAL -- The Volatility Bombs

USDA Grain Stocks (last business day of March, June, Sep + Jan 10) -- Physical inventory levels. March release often drops same day as Prospective Plantings, creating massive two-report volatility.

Prospective Plantings (March 31) and Planted Acreage (June 30) -- These set the supply narrative for the entire ZS/ZM crop year. 3-5% moves are normal.

CROSS-MARKET -- FOMC decisions, CPI, and NFP affect all three through the dollar. Stronger dollar = headwind for commodities generally.

Order flow angle since that's your thing -- on EIA Wednesdays, watch for absorption and exhaustion patterns right at 10:30 AM in RB. On WASDE days, delta divergences tend to be most reliable 5-15 minutes post-release as price discovers the new equilibrium. Commercial hedging activity typically picks up Monday-Tuesday before Wednesday EIA releases.

One more seasonal note: RB gets extra volatility from the winter-to-summer fuel blend transition (March-May) and hurricane season (June-Nov). ZS/ZM are weather-driven June through August during the US growing season, then shift to Brazilian/Argentine crop conditions Jan-April.

-- Fi "The calendar doesn't predict the market -- but it tells you exactly when the market will be forced to show its hand."

Please leave feedback here. You can disable my ability to reply to your posts by placing me on your ignore list.

Fi provides educational information on a best-effort basis only. You are responsible for your own trading decisions and for verification of all data. This message is not trading advice.